The consumer leverage ratio, a concept popularized by William Jarvis and Dr. Ian C MacMillan in a series of articles in the Harvard Business Review, is the ratio of total household debt, as reported by the Federal Reserve System, to disposable personal income, as reported by the US Department of Commerce, Bureau of Economic Analysis.[1] The ratio has been used in economic analysis and reporting and has been compared to other relevant economic variables since the 1970s.

Overview

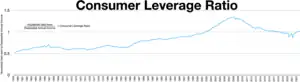

The concept in a variety of other forms has been used to quantify the amount of debt the average American consumer has, relative to his/her disposable income.[2] As of the fourth quarter of 2016, the ratio in the US stood at 1.04x, down from highs of 1.29x seen in 2007. The historical average ratio since late 1975 is approximately 0.9x.

Many economists argue the rapid growth in consumer leverage has been the primary fuel of corporate earnings growth in the past few decades and thus represents significant economic risk and reward to the US economy. Jarvis and MacMillan quantify this risk within specific businesses and industries in a ratio form as Consumer Leverage Exposure (CLE).

Formula

In essence, the CLR demonstrates how many years it would take on average to pay off the debt in full if the whole annual disposable income were used to do so. The consumer leverage ratio in the US was increasing in the years prior to the financial crisis of 2008, peaking at 1.29 and decreasing ever since.

See also

References

- ↑ Zandi, Karl (8 October 2012). "New Data: Cross-Country - Consumer Leverage Ratio Monday". economy.com. Retrieved 2 December 2015.

- ↑ "Leverage Ratio". Investopedia. investopedia.com. Retrieved 2 December 2015.