Debt crisis is a situation in which a government (nation, state/province, county, or city etc.) loses the ability of paying back its governmental debt. When the expenditures of a government are more than its tax revenues for a prolonged period, the government may enter into a debt crisis. Various forms of governments finance their expenditures primarily by raising money through taxation. When tax revenues are insufficient, the government can make up the difference by issuing debt.[1]

A debt crisis can also refer to a general term for a proliferation of massive public debt relative to tax revenues, especially in reference to Latin American countries during the 1980s, the United States and the European Union since the mid-2000s, and the Chinese debt crises of 2015.[2][3][4][5][6]

Debt wall

Hitting the debt wall is a dire financial situation that can occur when a nation depends on foreign debt and/or investment to subsidize their budget and then commercial deficits stop being the recipient of foreign capital flows. The lack of foreign capital flows reduces the demand for the local currency. The increased supply of currency coupled with an increased demand then causes a significant devaluation of the currency. This hurts the industrial base of the country since it can no longer afford to buy those imported supplies needed for production. Further, any obligations in foreign currency are now significantly more expensive to service both for the government and businesses.

This same concept has also been applied to personal debt. Specifically it has been applied to students who get in over their heads with student loans to finance their education.

Current and recent debt crises

Europe

European debt crisis

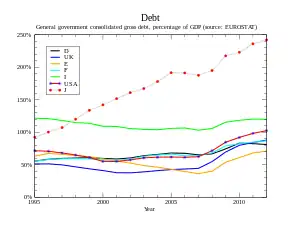

The European debt crisis is a crisis affecting several eurozone countries since the end of 2009.[7][8] Member states affected by this crisis were unable to repay their government debt or to bail out indebted financial institutions without the assistance of third-parties (namely the International Monetary Fund, European Commission, and the European Central Bank). The causes of the crisis included high-risk lending and borrowing practices, burst real estate bubbles, and hefty deficit spending.[9] As a result, investors have reduced their exposure to European investment products, and the value of the Euro has decreased.[10]

In 2007 the global financial crisis began with a crisis in the subprime mortgage market in the United States, and developed into a full-blown international banking crisis with the collapse of the investment bank Lehman Brothers on 15 September 2008.[11] The crisis was nonetheless followed by a global economic downturn, the Great Recession. The European debt crisis, a crisis in the banking system of the European countries using the euro, followed later.

In sovereign debt markets of PIIGS (Portugal, Ireland, Italy, Greece, Spain) created unprecedented funding pressure that spread to the national banks of the euro-zone countries and the European Central Bank (ECB) in 2010. The PIIGS announced strong fiscal reforms and austerity measures, but toward the end of the year, the euro once again suffered from stress.[12]

Causes

The eurozone crisis resulted from the structural problem of the eurozone and a combination of complex factors, including the globalisation of finance, easy credit conditions during the 2002–2008 period that encouraged high-risk lending and borrowing practices, the financial crisis of 2007–08, international trade imbalances, real estate bubbles that have since burst; the Great Recession of 2008–2012, fiscal policy choices related to government revenues and expenses, and approaches used by states to bail out troubled banking industries and private bondholders, assuming private debt burdens or socializing losses.

In 1992, members of the European Union signed the Maastricht Treaty, under which they pledged to limit their deficit spending and debt levels. However, in the early 2000s, some EU member states were failing to stay within the confines of the Maastricht criteria and turned to securitising future government revenues to reduce their debts and/or deficits, sidestepping best practice and ignoring international standards.[13] This allowed the sovereigns to mask their deficit and debt levels through a combination of techniques, including inconsistent accounting, off-balance-sheet transactions, and the use of complex currency and credit derivatives structures.[13]

From late 2009 on, after Greece's newly elected, PASOK government stopped masking its true indebtedness and budget deficit, fears of sovereign defaults in certain European states developed in the public, and the government debt of several states was downgraded. The crisis subsequently spread to Ireland and Portugal, while raising concerns about Italy, Spain, and the European banking system, and more fundamental imbalances within the eurozone.[14]

Other European debt crises

Greek debt crisis

Timeline of Greek debt crisis

2009 December - One of the world's three leading rating agencies downgrades Greece's credit rating amid fears the government could default on its ballooning debt. PM Papandrou announces programme of tough public spending cuts.

2010 January–March - Two more rounds of tough austerity measures are announced by government, and government faces mass protests and strikes.[15]

2010 April–May - The deficit was estimated that up to 70% of Greek government bonds were held by foreign investors, primarily banks.[16] After publication of GDP data which showed an intermittent period of recession starting in 2007,[17] credit rating agencies then downgraded Greek bonds to junk status in late April 2010. On 1 May 2010, the Greek government announced a series of austerity measures.[18]

2011 July – November - The debt crisis deepens. All three main credit ratings agencies cut Greece's to a level associated with substantial risk of default. In November 2011, Greece faced with a storm of criticism over his referendum plan, Mr Papandreou withdraws it and then announces his resignation.[15]

2012 February - December - The second bailout programme was ratified in February 2012. A total of €240 billion was to be transferred in regular tranches through December 2014. The recession worsened and the government continued to dither over bailout program implementation. In December 2012 the Troika provided Greece with more debt relief, while the IMF extended an extra €8.2bn of loans to be transferred from January 2015 to March 2016.

2014 - In 2014 the outlook for the Greek economy was optimistic. The government predicted a structural surplus in 2014,[19] opening access to the private lending market to the extent that its entire financing gap for 2014 was covered via private bond sales.[20]

2015 June – July - The Greek parliament approved the referendum with no interim bailout agreement. Many Greeks continued to withdraw cash from their accounts fearing that capital controls would soon be invoked. On 13 July, after 17 hours of negotiations, Eurozone leaders reached a provisional agreement on a third bailout programme, substantially the same as their June proposal. Many financial analysts, including the largest private holder of Greek debt, private equity firm manager, Paul Kazarian, found issue with its findings, citing it as a distortion of net debt position.[21][22]

2017 - The Greek finance ministry reported that the government's debt load is now €226.36 billion after increasing by €2.65 billion in the previous quarter.[23] In June 2017, news reports indicated that the "crushing debt burden" had not been alleviated and that Greece was at the risk of defaulting on some payments.[24]

2018 - Greek successfully exited (as declared) the bailouts on 20 August 2018.[25]

Greek debt restructuring

It stands out in the history of sovereign defaults. Greek debt restructuring of 2012 achieved very large debt relief – with minimal financial disruption, using a combination of new legal techniques, exceptionally large cash incentives, and official sector pressure on key creditors. But it did so at a cost. The timing and design of the restructuring left money on the table from the perspective of Greece, set precedents and created a large risk for taxpayer – particularly in its very generous treatment of holdout creditors – that are likely to make future debt restructurings in Europe more difficult.[26]

Effects

To take considerations that the most characteristic feature of the Greek social landscape in the current crisis is the steep rise in joblessness. The unemployment rate had fluctuated around the 10 per cent mark in the first half of the previous decade. It then began to fall until May 2008, when unemployment figures reached their lowest level for over a decade (325,000 workers or 6.6 per cent of the labour force). While job losses involved an unusually high number of workers, loss of earnings for those still in employment was also significant. Average real gross earnings for employees have lost more ground since the onset of the crisis than they gained in the nine years before that.[27]

In February 2012, it was reported that 20,000 Greeks had been made homeless during the preceding year, and that 20 per cent of shops in the historic city centre of Athens were empty.[28]

Latin America

Argentine debt crisis

Background

Argentina's turbulent economic history: Argentina has a history of chronic economic, monetary and political problems. Economic reforms of the 1990s. In 1989, Carlos Menem became president. After some fumbling, he adopted a free-market approach that reduced the burden of government by privatizing, deregulating, cutting some tax rates, and reforming the state. The centerpiece of Menem's policies was the Convertibility Law, which took effect on 1 April 1991. Argentina's reforms were faster and deeper than any country of the time outside the former communist bloc. Real GDP grew more than 10 percent a year in 1991 and 1992, before slowing to a more normal rate of slightly below 6 percent in 1993 and 1994. [29]

The 1998–2002 Argentine great depression was an economic depression in Argentina, which began in the third quarter of 1998 and lasted until the second quarter of 2002.[29][30][31][32][33][34] It almost immediately followed the 1974–1990 Great Depression after a brief period of rapid economic growth.[33]

Effects

Several thousand homeless and jobless Argentines found work as cartoneros, cardboard collectors. An estimate in 2003 had 30,000 to 40,000 people scavenging the streets for cardboard to sell to recycling plants. Such desperate measures were common because of the unemployment rate, nearly 25%.[35]

Argentine agricultural products were rejected in some international markets for fear that they might have been damaged by the chaos. The US Department of Agriculture put restrictions on Argentine food and drug exports.[33]

Debt restructuring history

2005 Venezuela was one of the largest single investors in Argentine bonds following these developments, which bought a total of more than $5 billion in restructured Argentine bonds from 2005 to 2007.[36] Between 2001 and 2006, Venezuela was the largest single buyer of Argentina's debt. In 2005 and 2006, Banco Occidental de Descuento and Fondo Común, owned by Venezuelan bankers Victor Vargas Irausquin and Victor Gill Ramirez respectively, bought most of Argentina's outstanding bonds and resold them on to the market.[37] The banks bought $100 million worth of Argentine bonds and resold the bonds for a profit of approximately $17 million.[38] People who criticize Vargas have said that he made a $1 billion "backroom deal" with swaps of Argentine bonds as a sign of his friendship with Chavez.[39] The Financial Times interviewed financial analysts in the United States who said that the banks profited from the resale of the bonds; the Venezuelan government did not profit.[38]

Bondholders who had accepted the 2005 swap (three out of four did so) saw the value of their bonds rise 90% by 2012, and these continued to rise strongly during 2013.[40]

2010 On 15 April 2010, the debt exchange was re-opened to bondholders who rejected the 2005 swap; 67% of these latter accepted the swap, leaving 7% as holdouts.[41] Holdouts continued to put pressure on the government by attempting to seize Argentine assets abroad,[42] and by suing to attach future Argentine payments on restructured debt to receive better treatment than cooperating creditors.[43][44][45]

The government reached an agreement in 2005 by which 76% of the defaulted bonds were exchanged for other bonds at a nominal value of 25 to 35% of the original and at longer terms. A second debt restructuring in 2010 brought the percentage of bonds out of default to 93%, but some creditors have still not been paid.[46][47] Foreign currency denominated debt thus fell as a percentage of GDP from 150% in 2003 to 8.3% in 2013.[48]

U.S. interventions

The U.S. foreign policy known as the Roosevelt Corollary asserted that the United States would intervene on behalf of European countries to avoid those countries intervening militarily to press their interests, including repayment of debts. This policy was used to justify interventions in the early 1900s in Venezuela, Cuba, Nicaragua, Haiti, and the Dominican Republic (1916–1924).

North America

See also

Further reading

- World Bank, 2019. Global Waves of Debt: Causes and Consequences. Edited by M. Ayhan Kose, Peter Nagle, Franziska Ohnsorge, and Naotaka Sugawara.

References

- ↑ Bondarenko, Peter (September 2015). "Debt crisis". Encyclopædia Britannica. Retrieved 29 March 2019.

- ↑ Jetin Duceux, Alice (December 2018). "An overview of Chinese Debt (Part 1)". CADTM.

- ↑ ""Europe Banks Selling Sovereign Bonds May Worsen Debt Crisis" - SFGate". Archived from the original on 10 May 2020. Retrieved 19 November 2011.

- ↑ "Who is Handling Debt Crisis Better, United States or Europe" - US News

- ↑ Marsh, Bill (May 1, 2010). "Europe's Web of Debt". The New York Times.

- ↑ "How's the Argentina Recovery Coming Along?" by Tyler Cowen

- ↑ "Timeline: The unfolding eurozone crisis". BBC News. 13 June 2012. Retrieved 6 March 2015.

- ↑ Blundell-Wignall, Adrian (2011). "Solving the Financial and Sovereign Debt crisis" (PDF). Organisation for Economic Co-operation and Development. Retrieved 6 March 2015.

- ↑ Brown, Mark; Chambers, Alex (September 2005). "How Europe's governments have enronized their debts". Euromoney. Retrieved 6 March 2015.

- ↑ Johnson, Steve (1 March 2015). "Investors slash exposure to the euro". Financial Times. Retrieved 6 March 2015.

- ↑ Williams, Mark (12 April 2010). Uncontrolled Risk. McGraw-Hill Education. ISBN 978-0-07-163829-6.

- ↑ Clark, Janet H. (14 December 2010). "The Debt Crisis in the Euro Zone". Encyclopædia Britannica. Retrieved 29 March 2019.

- 1 2 "How Europe's Governments have Enronized their debts", Mark Brown and Alex Chambers, Euromoney, September 2005

- ↑ Paul Belkin, Martin A. Weiss, Rebecca M. Nelson and Darek E. Mix "The Eurozone Crisis: Overview and Issues For Congress", Congressional Research Service Report R42377, 29 February 2012.

- 1 2 "Greece profile-Timeline". BBC. 10 July 2010. Retrieved 2 April 2019.

- ↑ "Greece's sovereign-debt crisis: Still in a spin". The Economist. 15 April 2010. Retrieved 2 April 2019.

- ↑ "Quarterly National Accounts: 3rd Quarter 2014 (Flash Estimates) and revised data 1995 Q1-2014 Q2" (PDF). Hellenic Statistical Authority (ELSTAT). 14 November 2014. Archived from the original (PDF) on 14 November 2014.

- ↑ "Fourth raft of new measures" (in Greek). In.gr. 2 May 2010. Archived from the original on 5 May 2010. Retrieved 6 May 2010.

- ↑ "Greek economy to grow by 2.9 pct in 2015, draft budget". Newsbomb.gr. 6 October 2014.

- ↑ "Greece plans new bond sales and confirms growth target for next year". Irish Independent. 6 October 2014.

- ↑ "Investor Paul Kazarian returns with campaign for 'five-star' finance minister, Ilias Bellos | Kathimerini". Retrieved 2 April 2019.

- ↑ Chrysopoulos, Philip (10 December 2016). "Paul Kazarian: Greece's Largest Private Debt Owner Says Greek Debt Is Lower Than We Think [video] | GreekReporter.com". Retrieved 2 April 2019.

- ↑ Jennifer Rankin; Helana Smith (20 February 2017). "Greece standoff over €86bn bailout eases after Brussels deal". The Guardian. Retrieved 2 April 2019.

- ↑ El-Erian, Mohamed (22 June 2017). "Greek debt: IMF and EU's quick fix isn't enough - Mohamed El-Erian". The Guardian.

- ↑ "Greece exits final bailout successfully: ESM". Reuters. 20 August 2018. Retrieved 2 April 2019.

- ↑ "The Greek debt restructuring: an autopsy". Oxford Journals. 1 July 2013. Archived from the original on 7 July 2015. Retrieved 2 April 2019.

- ↑ Matsaganis, Manos (November 2013). "The Greek Crisis: Social Impact and policy responses" (PDF). Friedrich Ebert Stiftung. Retrieved 2 April 2019.

- ↑ Kerin Hope (17 February 2012). "Grim effects of austerity show on Greek streets". Financial Times. Retrieved 19 February 2012.

At least I'm not starving, there are bakeries that give me something, and I can get leftover souvlaki [kebab] at a fast-food shop late at night," [one homeless Greek] said. "But there are many more of us now, so how long will that last?

- 1 2 Saxton, Jim (June 2003). "Argentina's Economic Crisis: Causes and Cures". Joint Economic Committee. Washington, D.C.: United States Congress. Archived from the original on 29 October 2013. Retrieved 23 September 2013.

In 1998, Argentina entered what turned out to be a four-year depression, during which its economy shrank 28 percent.

- ↑ Cibils, Alan B.; Weisbrot, Mark; Kar, Debayani (3 September 2002). "Argentina Since Default: The IMF and the Depression". Center for Economic and Policy Research. Retrieved 23 September 2013.

- ↑ "Argentina's collapse: Scraping through the great depression". The Economist. Rosario, Argentina. 30 May 2002. Archived from the original on 20 October 2013. Retrieved 13 April 2019.

- ↑ Schuler, Kurt (August 2005). "Ignorance and Influence: U.S. Economists on Argentina's Depression of 1998–2002". Intellectual Tyranny of the Status Quo. Econ Journal Watch. pp. 234–278. Archived from the original on 25 December 2013. Retrieved 13 April 2019.

- 1 2 3 Kehoe, Timothy J. "What Can We Learn from the 1998–2002 Depression in Argentina?" (PDF). Minneapolis: Federal Reserve Bank of Minneapolis. pp. 1, 5. Retrieved 13 April 2019.

, Argentina experienced what the government described as a "great depression"

- ↑ Pascoe, Thomas (2 October 2012). "Britain is following Argentina on the road to ruin". The Telegraph. London. Archived from the original on 4 October 2012.

,

- ↑ "Accommodating an army of garbage pickers". CNN.com. 26 March 2003. Archived from the original on 18 May 2004. Retrieved 13 June 2014.

- ↑ "Chavez keeps up South American energy diplomacy". Reuters. 8 August 2007.

- ↑ "Venezuelan banks enjoy treasuries windfall". Financial Times. 31 January 2006. Retrieved 7 May 2015.

- 1 2 Coronel, Gustavo (27 November 2006). "Corruption, Mismanagement, and Abuse of Power in HugoChávez's Venezuela (Development Policy Analysis)". Center for Global Liberty & Prosperity. Washington, D.C.: The Cato Institute. p. 7.

- ↑ Padgett, Tim (23 April 2009). "The Dead Polo Ponies and Their Millionaire Owner". Time. Retrieved 13 April 2019.

- ↑ "Argentina offers new swap in pragmatic Plan B". Latin Finance. 27 August 2013. Retrieved 13 April 2019.

- ↑ Wray, Richard (16 April 2010). "Argentina to repay 2001 debt as Greece struggles to avoid default". The Guardian. Retrieved 13 April 2019.

- ↑ "The real story behind the Argentine vessel in Ghana and how hedge funds tried to seize the presidential plane". Forbes.

- ↑ Eavis, Peter (25 February 2013). "Banks Fear Court Ruling in Argentina Bond Debt". The New York Times. Retrieved 13 April 2019.

- ↑ Arthur Phillips and Jake Johnston (2 April 2013). "Argentina vs. the Vultures: What You Need to Know". CEPR.

- ↑ "What Argentina's fight with holdout creditors is all about". Reuters. 22 February 2013.

- ↑ J.F.Hornbeck (6 February 2013). "Argentina's Defaulted Sovereign Debt: Dealing with the "Holdouts"" (PDF). Congressional Research Service.

- ↑ "Banks Fear Court Ruling in Argentina Bond Debt". The New York Times. 25 February 2013.

- ↑ "Argentina Seeks to Restructure Debt Held by Vulture Funds". IPS News. 29 August 2013.